Business Line of Credit

A business line of credit provides access to capital as needed, with interest charged only on the amount borrowed.

Qualifications for a

Business Line of Credit

1+ Year in Business

![]()

Assets or Collateral

What Is a Business Line of Credit?

Essential Requirements for Obtaining a Business Line of Credit

How Does a Business Line of Credit Work?

How Does a Revolving Line of Credit Work?

Small Business Credit Line Benefits

Lines of Credit Vs. Small Business Loans

Secured Vs. Unsecured Business Line of Credit

Business Credit Cards Vs. Business Line of Credit

How Can You Use Business Line of Credit Funds?

How Could You Benefit from a Business Line of Credit?

Understanding Interest Rates and Payments for a Business Line of Credit

Applying for a Business Line of Credit

What Is a Business Line of Credit?

What Is a Business Line of Credit?

A small business line of credit provides flexible access to cash as needed, allowing you to draw from your total credit limit for any business purpose and only pay interest on what you use.

With a revolving line of credit, more funds become available as you pay down your balance. Unlike selling equity, this type of financing lets you maintain full ownership, profits, and control of your business.

You can use it to bridge cash flow gaps during seasonal slumps or as a rainy day fund, with no restrictions on its use. A business line of credit can cover any costs or opportunities you encounter.

Apply Now

Essential Requirements for Obtaining a Business Line of Credit

Essential Requirements for Obtaining a Business Line of Credit

Wondering how to apply for a business line of credit? Different lenders have various qualifications, so your eligibility can vary depending on where you apply. Applying through a marketplace allows you to explore options from multiple lenders with a single application.

Banks and credit unions typically have more stringent qualifications, making it difficult to qualify if your business doesn’t have a perfect financial record. Even if your application is denied at a bank, you might still qualify based on your annual sales with an online lender.

Online lenders are a better option for securing a fast business line of credit. Their expedited underwriting processes can potentially provide funds within 24 hours.

Marketplaces like National are less demanding, focusing more on your business and opportunities rather than history and credit. Applying and qualifying for a business line of credit through our marketplace is straightforward and not time-consuming.

Business Line of Credit Application

Here’s the documentation you’ll generally need:

- Driver’s license

- Business bank statements (at least one year)

- Business credit score

- Financial statements

- Time in business

- Proof of ownership (K1, Schedule C, EIN, certificate of incorporation, etc.)

- Business tax returns

- Collateral (if secured)

- Cash flow statement

- Business plan

Some lenders may require additional documentation to determine your eligibility, but the above list includes the most commonly requested items.

Apply Now

How Does a Business Line of Credit Work?

How Does a Business Line of Credit Work?

Business lines of credit function like credit cards but are structured to better suit small business owners. They offer tax advantages since you can write off interest on a business credit line, unlike with a personal credit card.

How They Work

Once you qualify for a business line of credit, you’ll receive a total credit limit. You can draw as much or as little as you need from that limit in multiple installments, with no obligation to use the full amount.

You manage this online by logging into an account and transferring funds from your credit line to your business bank account.

As you repay your balance, additional funds become available for use. You only pay interest on the amount you draw, not the full credit limit. However, be aware that some lenders may charge a non-utilization fee if you don’t use the line. Always ask for clear information about any fees before signing an agreement and avoid any agreements without transparent terms.

Choosing the Right Line of Credit

The best business line of credit is one that fits your business and its future goals. Work with a reputable, transparent lender to ensure the financing aligns with your objectives and imposes no restrictions on your growth.

Documentation Needed

- Driver’s license

- Business bank statements (at least one year)

- Business credit score

- Financial statements

- Time in business

- Proof of ownership (K1, Schedule C, EIN, certificate of incorporation, etc.)

- Business tax returns

- Collateral (if secured)

- Cash flow statement

- Business plan

Some lenders may require additional documentation, but the above list includes the most commonly requested items.

How Does a Revolving Line of Credit Work?

How Does a Revolving Line of Credit Work?

Unlike small business loans, revolving lines of credit work by allowing you to continue accessing additional funds as you pay your balance down and require more cash. In other words, it is a type of loan in which the user can borrow up to their credit again once the debt is repaid.

Some business lines of credit are revolving, while others aren’t. When you discuss the terms of your agreement, be sure to ask questions and confirm whether or not your line of credit is revolving. Revolving lines of credit are the fastest and easiest way to access additional cash as your business grows. Once you pay down part of the balance, you can draw more cash without reapplying. It’s simple, fast, and easy, and your working capital won’t be limited to your checking account.

For example, say you qualify for a $100,000 line of credit. You borrow the full $100,000 and use the cash to grow your business. You then pay down $50,000 using the revenue you generate, putting both your balance and credit limit at $50,000. With $50,000 paid down, you now have the option to borrow an additional $50,000. There’s no set end date, either. As long as you keep your credit line active or continue drawing and paying it down, you can utilize a LOC for months or even years. If you’re not actively using it, though, your small business line of credit may expire.

A top business line of credit option is one that has exactly what you need. If you aren’t satisfied with the first offer, don’t worry – there’s always a better deal out there.

Small Business Credit Line Benefits

Small Business Credit Line Benefits

A business line of credit can be a powerful tool in your back pocket. The flexibility allows you to draw funds whenever you need them and stay one step ahead of the latest challenge in your business – a priceless opportunity for any entrepreneur. Here are a few of the many benefits of leveraging a business line of credit in your operation:

- Fast access to cash

- Only pay interest on what you draw

- Might not need to offer collateral

- Manage your working capital, short-term projects, and other expenses

- Strengthen your business credit

A business line of credit for new businesses can change the way they grow. With flexible access to capital, you can build out necessary areas of your business without jeopardizing cash flow.

Term loans, SBA loans, and other traditional financing products provide you with a set amount of money that you must repay throughout the term outlined by your lender. If you wind up needing more than you originally anticipated, you’ll have to take out an additional loan on top of your previous financing, which can quickly become difficult to manage.

A business line of credit is a way around this challenge – the structure allows you to draw as much as you need from your total credit line without having to worry about taking out additional financing to afford your growth plans.

Lines of Credit Vs. Small Business Loans

Lines of Credit Vs. Small Business Loans

What’s the difference between a line of credit and a small business loan? Both provide your business with the cash you need to grow, but the way these products are structured is different.

When you apply for a small business loan, you receive the full amount you qualify for in one lump sum deposit. A line of credit, on the other hand, offers more flexibility than most loans and cash advances. Instead, you have the option to draw cash in increments and continue drawing more until you reach your credit limit.

Typically, lines of credit have lower interest rates and closing costs, which can make them more cost-effective. Small business loans are the better choice when you’re taking on a huge project with defined expenses. Lines of credit can be better as a flexible backup to cover unexpected costs or as a backup for your bank account.

Choosing a business line of credit over another financing solution could also help you save money on interest. If you were to secure a term loan to meet your needs, you’d have to pay interest on the total borrowed amount, whereas you only pay on what you use with a business line of credit. Plus, making consistent, timely payments on your credit line will work to strengthen your business credit score, which is a priceless opportunity that all entrepreneurs should take advantage of.

How to get a business line of credit? Check that you meet the necessary requirements, then reach out to the experts at National Business Capital to explore the options you qualify for.

Secured Vs. Unsecured Business Line of Credit

Secured Vs. Unsecured Business Line of Credit

A business line of credit can either be secured or unsecured. The difference depends on whether or not your lender requires you to put up collateral.

Secured Lines of Credit:

- Backed by collateral

- Higher credit limits

- Lower interest rates

- Lender can seize the collateralized asset if borrower defaults on payments

Unsecured Lines of Credit:

- No collateral necessary

- Higher interest rates

- Lower credit limits

- Difficult approval process

Some lenders require that borrowers put up collateral, such as real estate, receivables, inventory, equipment, or their home, as a method of protecting themselves from financial loss if the borrower defaults. However, putting up your home as collateral puts both your personal and business lives at risk.

For this reason, it’s usually not a wise choice. Backing your financing with collateral simply gives the lender confidence in the event you default. Years ago, it was difficult for a small business owner to qualify for an unsecured line of credit, especially through traditional lenders.

Through the new world of online lending, small business owners can qualify for multiple unsecured lines of credit options and compare rates. While they don’t require collateral, unsecured options may have slightly higher rates due to the lender’s increased risk.

By putting up collateral and opting for a secured line of credit financing, you may qualify for a higher approval. That being said, you can usually still qualify for a competitive unsecured line of credit based only on your annual sales – even with personal credit challenges.

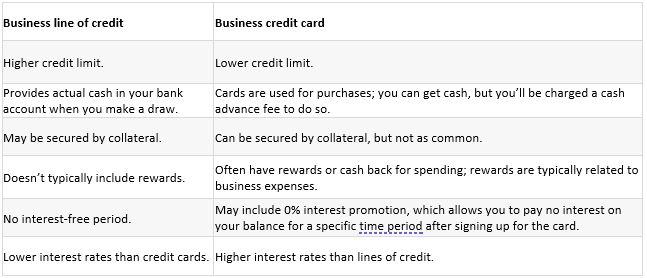

Business Credit Cards Vs. Business Line of Credit

Business Credit Cards Vs. Business Line of Credit

Fundamentally, credit cards and lines of credit are similar – they give you the ability to handle expenses when you need to.

Both financing products only charge interest on what you use rather than your total credit limit, but the interest is structured differently. A business line of credit is the ideal option for your small business if you’re growing or solving challenges and you need a lower-cost solution.

Usually, only about 3% of your minimum monthly credit card payment goes toward principal. Over time, this can add up to be quite expensive. Lines of credit typically have lower interest rates and better amortization schedules. Overall, this normally adds up to a lower total cost.

Credit cards are primarily transactional, meaning you can only use them to make purchases. It’s possible to borrow cash using a credit card, but this can be expensive. On the other hand, lines of credit give you the ability to instantly draw cash as you cover expenses and manage working capital.

If you’re debating between getting a credit card vs. a business line of credit, you should also consider fees. Some credit cards involve hefty interest rates. In most cases, these costs will outweigh the draw fees you may or may not pay with line of credit financing. If you opt for a business line of credit, you won’t accrue rewards like you would with a credit card.

However, you can maximize the value of both financing options by spending with your credit card to accumulate rewards, then paying the balance down with a line of credit. Using both has its advantages, but you should make sure that you’re choosing the best business line of credit and credit card for your business and where it’s headed by weighing out your options beforehand.

How Can You Use Business Line of Credit Funds?

How Can You Use Business Line of Credit Funds?

Lines of credit are intended to be flexible financing options custom-tailored to your needs. You can use them to cover expenses that are weighing your business down or pursue exciting new growth opportunities.

There are no restrictions on how you must spend this money – you can put it toward any expenses. Some of the most common ways that businesses utilize this business financing option include:

- Grow Your Business – Ramp up your business and cover the expenses needed to expand hiring, payroll, take on new jobs, and more.

- Operating Costs – Always have cash on hand for rent, utilities, and other costs required to keep your business going on a day-to-day basis.

- Marketing Campaigns – Drum up new business and take on more customers with additional marketing campaigns in the mix.

- Seasonal Slow Periods – Get the capital you need to keep your business moving during seasonal slow periods.

- Inventory or Supplies – Purchase additional inventory or supplies to capitalize on busy periods and new opportunities.

- Payroll – Keep a reservoir of funding to cover the costs of payroll, especially with slow-paying clients.

Access to a line of credit is like having cash on demand. The second you need cash, you can draw from your line of credit and get things moving.

You may also have to provide a personal guarantee, which is standard with most types of business financing, and is similar to a personal guarantee you already have with your credit cards.

How Could You Benefit from a Business Line of Credit?

How Could You Benefit from a Business Line of Credit?

What would you do if an opportunity to grow your business came along during your slow season? If you didn’t have the cash flow to take advantage of it, would you let the opportunity pass you by?

Business lines of credit make your opportunities attainable. You can quickly access funds, repay over an extended schedule, and enjoy a favorable interest format that allows you to keep your financing on the sidelines when you need it. Entrepreneurs with lines of credit commonly say that their cash flow and operations are more streamlined now that they have the right capital source in place.

Understanding Interest Rates and Payments for a Business Line of Credit

Understanding Interest Rates and Payments for a Business Line of Credit

Most business owners prefer a line of credit over other options because of how interest rates are structured. Rather than charging on the total approval amount, you’ll only pay interest on what you take.

- Using the previous example, let’s say you qualify for a $100,000 business line of credit at a 6% interest rate and draw $50,000. You’d be charged interest only on the principal, which is the $50,000 you drew and not the $100,000 you were approved for.

- The interest would be amortized over 12 months. Typically, in this example, your total interest paid over the course of the term would be $3,000, but the payment structure can vary depending on your lender.

- Your monthly interest payments would be $3,000 divided by 12, which is $250 per month. You can find your expected monthly payments based on a fixed interest rate using our business line of credit calculator.

This structure allows you to keep your line of credit on the sidelines when you need it – without worrying about excessive interest.

Determining your specific interest rate isn’t as straightforward as the payment structure. Rates can depend on a number of factors, including your time in business, credit score, annual revenue, and the lender you’re working with. Still, that doesn’t mean you should settle for an interest rate that doesn’t fit your business.

You should apply with multiple lenders to ensure you’re getting the best deal available. If you apply for a business line of credit online, the application process is much easier than dealing with that of a bank or credit union.

Applying through direct lenders one by one limits the options you could potentially qualify for, while applying at a marketplace leaves the door open to several potential options, ensuring you find the best one.

Applying for a Business Line of Credit

Applying for a Business Line of Credit

Applying for a line of credit is easy, and simply learning your options won’t affect your credit score. Here’s how it works:

Apply

Fill out our simple 60-second application to begin the process. Then, complete your online application by connecting your bank statements through our bank-grade portal in under 3 minutes.

Review

Consider multiple loan options available within our marketplace. Hear your options explained by a knowledgeable Business Financing Advisor, and ask any questions you have.

Get Funded

Select the best option available and get funded in as little as a few hours. Start using your cash to grow your business right away, without restrictions on how you can use the funds.

We educate you on the best options available within our platform to ensure you get the best line of credit available.

Lowest Rates, Longest Terms, & Highest Amounts

Funding Amount

Up to $100MM

Repayment

Up to 25 years

Time to Fund

1 to 7 days

Questions to Ask Before Applying for a Business Line of Credit

Questions to Ask Before Applying for a Business Line of Credit

You only pay on the amount you draw – not your total credit line. That means that – if you draw $50,000 from your $100,000 credit line – you’re only paying interest on the $50,000.

This structure allows you to keep your line of credit on the sideline for when you need it without worrying about unnecessary interest.

Can a Business Line of Credit Improve My Business Credit Scores?

If your lender reports to a business credit bureau, then timely and consistent payments will work toward strengthening your credit score. Otherwise, your timely repayment will build “credibility” and “creditworthiness” with your lender, which can help you secure better terms in the future.

What Is the Average Interest Rate for a Business Line of Credit?

Interest rates range from 5% to 60%, depending on your business credit score, annual revenue, your time in business, and your willingness/ability to offer collateral.

Collateral, which can be equipment, real estate, or strong receivables, serves as an extra layer of protection against defaults for the lender. By offering an asset to secure your financing, you reduce the level of risk for the lender and, in turn, decrease the interest rate you’ll receive.

Can I Get a Business Line of Credit With Bad Credit?

Yes, you can secure a business line of credit with a lower FICO score, but you should also be realistic about the terms you qualify for.

Lower FICO scores are seen as “risky” by lenders, so they’ll offer higher interest rates and lower credit limits as a result. You may have to offer collateral, too, as a method of securing the financing.

If your credit score is less than favorable, it’s worthwhile to consider proactively strengthening it before applying for financing. Not everyone has enough time to do this, of course, but even minor increases can yield big savings when it comes to interest rates.

Unsecured vs. Secured Lines of Credit: What’s the Difference?

Unsecured lines of credit require no collateral backing, whereas a secured line of credit comes with a collateral requirement. If you default on secured financing, the lender can seize the collateralized assets to recoup their lost cost.

Although unsecured credit lines don’t need collateral, some lenders require a personal guarantee or lien to approve your application. These give your lender the right to target your personal assets if you’re unable to repay your loan.

It’s important to understand whether your contract requires collateral, a personal guarantee, or a lien before you finalize it. Never be afraid to ask your lender questions or walk away if a contract doesn’t make sense.

How to Get a Business Line of Credit?

If you’re looking to get a business line of credit, you’ll need to approach the situation strategically. Here are some steps to take.

- Evaluate Your Funding Need: First and foremost, you’ll need to understand why you need business funding and how fast you need it to meet your goals. You should also review your business finances and determine a safe level of debt to take on.

- Review Lender Requirements: From one to another, each lender has different requirements, preferred industries, and nuances that affect your benefits. Understand the qualifications of multiple lenders, so you can apply with more than one and give yourself options to choose from.

- Proactively Gather Documentation: Coming prepared with all the information your lender needs is one of the best ways to speed up the funding process. If you’re unsure of what documents you need to bring, don’t be afraid to reach out directly to the lender and ask.

- Apply and Compare Your Options: Once you have a list of a few top lenders where you either meet or exceed the minimum qualifications, you’ll apply with each and compare your approvals. Having options at this stage gives you negotiating power, which can serve to improve your offered terms.

At National Business Capital, you can simplify the process above and gain a financing partner simultaneously. With one easy application, you unlock all the most competitive offers you qualify for within our diverse lender platform. Your personal Business Finance Advisor helps you select the best one with your best interest placed at the forefront.

Is a Bank Line of Credit Better Than a Credit Card?

Although your specific interest rate depends on a variety of factors, business lines of credit generally carry lesser interest rates than business credit cards. They also feature higher credit limits, which allows borrowers an entirely different level of flexibility and financial power.

Is a Line of Credit Better Than a Business Loan?

It all depends on your business and goals. For some, the flexibility of a line of credit makes it a better option than a business loan, while others prefer the lump sum format of standard term loans.

There are many businesses that need a specific format of credit. For example, a business seeking to begin a major renovation of multiple storefronts would benefit more from a longer-term, more substantial lump-sum product. If they had leveraged a business line of credit, they’d likely have their entire line drawn, which would significantly raise what they’re paying in interest.

If you’re unsure of which financing option is right for your unique circumstances, our Business Finance Advisors can help. Complete our digital application today to start the process with our team.

What Are the Business Line of Credit Benefits?

Here are a few of the many benefits of a business line of credit.

- Flexible access to capital

- Streamlined cash flow

- Interest applies only to the amount drawn

- Can build business credit/creditworthiness

- Easy to use

- Ability to use the financing as an emergency fund

The flexibility of business lines of credit is the most prominent benefit. Unlike other financing options, you’re able to draw funds whenever necessary and enjoy an extended repayment schedule.

Secure the Best Business Line of Credit in 2024

-

Paperwork

-

Application

- Number of Lenders

- Service Level

- Approval Process

- Speed to Funding

- Collateral Requirements

- Business Profitability

- Credit Score

- Credit Check

Successful Funds

-

3 Months Bank Statements

No Tax Returns Required -

One Page – One Minute

DocuSign - 75+

- Business Advisor

- Hours/Days

- Hours/Days

- Not Necessary

- Not Necessary

- No Minimum FICO

- Soft Pull

Apply Now

Terms & Conditions apply

Best

Bank

-

2-3 Years Tax Return

2-3 Years Financials -

Lengthy

Paper Intensive - 1

- Processor

- Weeks/Months

- Months

- Always

- Last 2 Years

- 680+ FICO

- Hard Pull

Direct Lenders

-

2-3 Years Tax Return

2-3 Years Financials -

Lengthy

Paper Intensive - 1

- Processor

- Weeks/Months

- Months

- Always

- Last 2 Years

- 680+ FICO

- Hard Pull